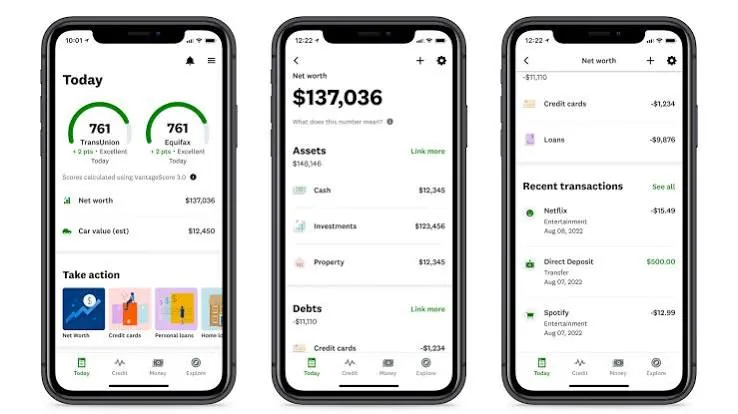

Credit Karma is accurate for what it actually shows: real credit data pulled directly from TransUnion and Equifax. The catch is the score number itself, which can differ meaningfully from what lenders see, because Credit Karma uses a different scoring model than most banks.

Trust Credit Karma for the report data (accounts, balances, payment history, inquiries) and for tracking whether your credit is trending up or down. Don’t treat the number as the score a lender will pull. Credit Karma shows VantageScore 3.0, while most lending decisions rely on a FICO model, and the two commonly differ by 20 points or more.

Reviewed by Alessandro Mirani · Last reviewed July 1, 2026. This article explains how Credit Karma’s scores and monitoring work and where they differ from lender scoring. It is general information, not financial advice.

The core issue: VantageScore vs. FICO

Credit Karma uses VantageScore 3.0, not FICO. Both models use the same 300–850 range, which makes them look interchangeable, but they weight factors differently and can produce materially different results:

- The typical gap is commonly around 20–25 points, sometimes more.

- In extreme cases, users have reported differences of more than 100 points (for example, a Credit Karma score of 630 alongside a FICO in the 720–730 range).

- One user tracking multiple platforms reported Credit Karma showing 809 while a FICO 8 from the same bureau showed 766.

- According to FICO, over 90% of top lending decisions use a FICO score, especially for mortgages and auto loans, not VantageScore.

What Credit Karma gets right

- Credit report data is accurate. Accounts, balances, payment history, and hard inquiries come from real TransUnion and Equifax bureau data.

- Trend tracking. It’s genuinely useful for watching whether your score is moving up or down over time.

- Account monitoring. It reports the exact dates when creditors report balances to the bureaus, which most other free tools don’t show.

- New accounts and inquiries. It alerts you quickly when something new appears on your report.

That last point matters more than most people think. With large-scale incidents like the AT&T data breach exposing personal data, and fraud trends in 2026 leaning heavily on identity abuse, a free tool that flags a new account you didn’t open is a real early-warning system. Pair it with cleaning your details off people-search sites like USPhoneBook and staying alert to payment app scams, and you’ve covered the basics of identity protection without spending anything.

Where it falls short

| Limitation | Detail |

|---|---|

| Missing Experian | Only shows 2 of 3 bureaus; Experian data is absent entirely |

| Score inflation | VantageScore often runs higher than FICO, which can give false confidence before applying for credit |

| Old derogatory marks | May show “100% on-time payments” even if a late payment exists from 5+ years ago; FICO still weighs those heavily |

| “Pre-approved” offers | Approval Odds are not guarantees; they’re based on comparisons with other Credit Karma members, not lender criteria |

| Score model mismatch | Lenders use many FICO versions (FICO 8, FICO 9, FICO Auto, FICO Mortgage); Credit Karma shows none of them |

Bottom line: when to use it (and when not to)

Use Credit Karma for:

- Free ongoing credit monitoring

- Spotting errors or fraudulent accounts on your TransUnion and Equifax reports

- Tracking progress trends over months

Don’t rely on it for:

- Predicting approval or rates before a mortgage, auto loan, or any serious credit application

- Assuming the number is your “real” credit score

For lending decisions, check your actual FICO score through Experian (free tier available), myFICO, or directly through your bank or credit card issuer, since many provide free FICO scores. You can also pull your full reports from all three bureaus at no cost through AnnualCreditReport.com, the official source authorized by US federal law.

Frequently asked questions

Is Credit Karma’s score my real credit score?

It’s a real score, calculated from real TransUnion and Equifax data, but it’s a VantageScore 3.0. Most lenders pull a FICO score instead, so the number you see on Credit Karma is usually not the number a lender sees.

Why is my Credit Karma score different from my FICO score?

VantageScore and FICO weight factors differently, even though both use the 300–850 range. The gap is commonly around 20–25 points, and in some reported cases it exceeds 100 points.

Does Credit Karma show all three credit bureaus?

No. Credit Karma shows TransUnion and Equifax only. Anything that appears solely on your Experian report won’t show up at all.

Are Credit Karma’s Approval Odds reliable?

Treat them as rough estimates, not guarantees. They’re based on comparisons with other Credit Karma members with similar profiles, not on the actual criteria a specific lender uses.

Where can I see the score lenders actually use?

Check Experian’s free tier, myFICO, or your own bank or credit card issuer, since many now include a free FICO score. Before a major application like a mortgage, ask the lender which score model they pull.

This article is general information, not financial advice. Credit scoring models, lender practices, and Credit Karma’s features change over time; verify current details with the lender or service directly before making financial decisions.